This blog is devoted to investor education. Our aim is to provide here best advice to help you to make investment decisions to grow your wealth.

Search This Blog

Wednesday, 27 December 2017

Investment tips for new employees

Dreams, these days, come with a high price tag. A car for Rs 5 lakh, a house for Rs 50 lakh, several lakhs for a decent education for kids and crores for a cushy retirement. In fact, seemingly simple needs have been elevated to dreams due to the high cost associated with them. You require either a large income or a strategic plan to meet these basic life goals. While the former may not always be easy for the average salaried person, the latter is certainly within reach, especially if you begin at the beginning. Make a financial plan the day you start working and you won't have to scramble to fund each aspiration.

However, it may not be as easy as it seems. "I just don't know how much to save and where to invest, so I don't budget and end up spending a lot," says Harshinder Kaur, who started working two years ago as a probationary officer at a bank in Ganganagar, Rajasthan. She doesn't know how to formulate a plan for herself. This is a predicament many youngsters in their mid-20s face. The twin behavioural devils of ignorance and procrastination push most people into their 30s before they get down to streamlining their finances. This often results in faulty investment choices, flawed portfolios, unmet goals and financial insecurity later in life. "This category is not a cash cow for advisory firms, and as they have no one to turn to, they often get lost," says Jayant Pai, CFP and Head, Marketing, PPFAS Mutual Fund. We, at ET Wealth, will try to remedy this through our cover story this week. In the following pages, we offer the newly employed youth a step by step guide to plan their finances. We focus on the building blocks they need at this stage: budgeting, goals, investment, insurance, taxation and salary structure. However, this is merely intended to propel them into planning and they will need to research and learn continuously throughout their working lives. Remember, financial freedom is not achieved the day you start working, but the day you get your finances in working order.

Also Read: Young earner? Five financial mistakes you may regret later 1. MAKE A BUDGET & START SAVING Budgeting is the simple exercise of reconciling your income with your expenses, and should be your first step. Note down your monthly spending as per your ease of usage: Excel sheet, simple diary, mobile app, or desktop. The aim is to know how much you spend under various heads. "I use Excel sheet to keep track of my spending and know what percentage of my salary goes where," says 24-year-old Saugata Palit, who has been working as senior executive in a private firm in Delhi for the past 18 months.

After you have budgeted for 3-4 months, you will realise that your expenses can be sorted into three categories: essential, discretionary and entertainment. "Tracking of budget is important not only to identify mandatory and discretionary spends, but also ensure that you don't overspend," says Vinit Iyer, CFP & Founder, Wealth Creators Financial Advisors. Once you've identified the outgoing amount, put away 10-20% of your salary every month before you start spending. If you don't know where to put it, start with your bank account. Try to opt for a sweep-in account that has a fixed deposit linked to it as it will fetch you a rate higher than 4%, which you get from your savings account. This will help inculcate a lifelong saving habit and make sure that you money starts to work for you immediately. As financial planner Pankaaj Maalde says, "It's important that your money does not lie idle." This is because with very few liabilities and responsibilities, this is the ideal period to save and take advantage of the power of compounding. The earlier you start saving, even if it is a small amount, the more time your money will have to grow. Even as you start saving, another first is to start educating yourself about every aspect of personal finance. "Read articles and books to understand concepts like saving, investing, protection, debt, inflation, compounding, etc, and how these are intertwined," says Pai. The more informed you are, the better your decision-making. Also Read: Do you know your financial personality? Take this quiz! 2. FRAME YOUR FINANCIAL GOALS You have started saving, but will you have enough to buy a house 10 years down the line, or even a car five years hence? People tend to save aggressively and invest with extreme vigour, but do so blindly, jeopardising their goals. This is a mistake common to most investors, irrespective of the age group. The next step then is to frame your goals. Don't just make a mental note of the things you want to finance, but write these down in detail. Split your goals into three categories: short-, medium- and long-term goals. Then list each one clearly, along with the number of years to achieve each, and the exact amount you will need. Once you have penned down your goals, you will be able to determine how much and for how long you will need to invest. Don't forget to factor in inflation while calculating the amount since it will shoot up the value of your goal. If you decide to buy a car that costs Rs 5 lakh today after seven years, it will cost you Rs 8.5 lakh if you consider 8% inflation. Similarly, the post-tax returns from a fixed deposit that offers 7.5% return may not be able to beat the rise in prices over the long term.

While Palit manages to save 29% of his salary each month and has also framed short-term goals, he hasn't factored in inflation, nor the corpus he will manage to build. There are other things you need to consider while deciding goals. "The nature of your income, earning capacity in the coming years, dependants, loans and personal priorities must essentially be considered while framing goals," says Pai. Also remember that these milestones may alter somewhat with your changing circumstances, say, after getting married or having children. You will then have to make the necessary adjustments. If you think you cannot do so on your own, take the help of a financial adviser who takes into account your specific needs and wants. Also Read: Young earner? Five financial mistakes you may regret later 3. INVEST IN RIGHT INSTRUMENTS The biggest dilemma that young earners face is where to invest their money. "To start with, just choose simple instruments like a recurring or fixed deposit. Once you have prioritised your goals, then think about converting your savings to investments," says Maalde. "If you are not familiar with instruments, pick options that are readily available, say, in a bank, and offer liquidity," adds Iyer. Essentially, the investment vehicle should be chosen in line with your goals and time horizon. "If it's a short-term goal, keep it in debt; if it's for the long term, it should be mandatorily equity," says Kartik Jhaveri, Director, Transcend Consulting. The medium-term goals should have a mix of debt and equity. This is because debt will offer you the safety of capital since you need it in the short term, while equity has historically given the highest returns in the long term. This is a simple generalisation, but as you have just started earning and are not familiar with the investing territory, go for it till you are better informed. Then take into consideration other factors like returns, liquidity and tax liability before choosing an asset class. For near-term goals, opt for recurring deposit, liquid funds, fixed deposit or short-term debt funds. For the medium-term, you could choose balanced funds and equitylinked saving schemes. For the long term, equity mutual funds, NPS, PPF and EPF could be your instruments of choice. Do not blindly take your parents' and well-wishers' advice, but conduct your own research. Bengaluru-based Siddhartha Nayyar, 23, is learning from experience. "I tried my hand at the stock market recently, but faced a loss. So I have backed off for now and will conduct proper research on stocks and mutual funds before trying again," says the project coordinator with a software firm. On the other hand, 24-year-old Dharma Teja is learning from observation. "When I saw my father's investment go up sharply with mutual funds, I decided to opt for it and am now investing my entire surplus of Rs 45,000 in equity funds," says the product manager with a private firm in Mumbai. He is, however, accumulating funds for short-term goals and should shift it to debt as he approaches the goal. At the other extreme is Palit, who has a 100% debt portfolio, with investments in recurring deposit, PPF and gold ETF. He should diversify into equity soon. Which investment should you pick? Consider the goal tenure, returns, taxation and liquidity before investing your hard earned money.

Also Read: Should young earners take their parents' advice while investing? 4. MAXIMISE TAX SAVINGS Saving tax is not a priority for most new earners because the salary is not too high, nor the knowledge regarding taxability of instruments. "Do not be obsessed with investing just for saving tax as some expenditures may be useful," says Pai. However, it is important to brush up your tax awareness at the earliest. Start with avenues that offer tax deduction of Rs 1.5 lakh under Section 80C. Some of these include the EPF, PPF, NPS, 5-year tax-saving fixed deposits, ELSS, Ulips, life insurance, etc. Then opt for investments that fit in with your goals and needs, or those that are being made by default. The latter could include EPF or the NPS. "You could also use insurance and healthcarerelated expenses for dependants astutely," says Pai. These would include premium spent on health plans under Section 80D, which is up to Rs 25,000 for self and dependants, and Rs 30,000 for senior parents. "I only have a working knowledge of tax as it is not need of the hour for me. Still, I am saving tax through investments in the PPF and gold ETFs," says Palit. Another important thing is to calculate the returns from your investments after considering the tax. So Palit should undersrand that gold ETFs will invite short-term or longterm capital gains tax. You can also save tax by negotatiating with your employer for a a taxfriendly salary structure.

Siddhartha Nayyar, 23 years, Bengaluru Designation: Project Coordinator Started work at 21 years "I'm open to investing in mutual funds, but want to test my learning in the stock market."

Flying start 1. Has no loans; has repaid vehicle loan. 2. Pays credit card bills in full each month. 3. Working knowledge of taxation on investments. Take-off troubles 1. Fully invested in debt, no equity. 2. Low savings, high expenses. 3. Only employer's health cover. No other insurance. 5. OPT FOR THE RIGHT INSURANCE The basic purpose of insurance is to cover risks in your life, not offer returns. Still, most people confuse it with investment because of the products in the market that offer both. While you may not feel much need for any kind of cover when you are young, it's best to know about the various types at the start of your financial life. "The lure of tax saving and the urgency to get tax planning components in place at the end of financial year can push one to make unwise choices," says Antony Jacob, CEO, Apollo Munich Health Insurance. Life insurance The term plan offers a big cover for a small premium, but you do not get any returns. Then, there are traditional plans, which include endowment and moneyback policies. These offer small covers for a high premium, and low rates of return. Finally, there are Ulips, which are marketlinked insurance plans with a lockin period of five years and provide a low cover for a high premium, but offer market-linked returns. The last two are typically used The last two are typically used as a wealth creation tool because of returns, but remember that in case of traditional plans, the rate is low, usually 5-6%, and you can earn higher returns by investing in other instruments. Teja is paying a premium of Rs 25,000 a year for an endowment plan that was bought for him by his father even though he doesn't need it. At this point, the only life cover you may need is a term plan, but this too, only if you have financial dependants or large liabilities in the form of debt. Teja has a Rs 75 lakh term plan though he has no dependants or liabilities yet. Harshinder, on the other hand, has not bought any cover. "Since I am single and don't have any dependants or debt, I didn't think I needed any life cover," she says. Health insurance The broader categorisation includes the basic indemnity plan, which covers hospitalisation expenses, for an individual, and the family floater plan, which includes your entire family in a single cover. "Growing incidence of lifestyle diseases and rising medical costs make it essential to have a health insurance," says Ashish Mehrotra, CEO & MD, Max Bupa Health Insurance. "Also, a health plan provided by an employer may not be enough to hedge one against the rising cost of healthcare services," says Jacob. You should have Rs 3-5 lakh basic health plan at this stage, depending on whether you stay in a metro or a tier II/III city. So if your company insures you for Rs 2 lakh, buy an independent top-up plan for Rs 3 lakh as it will be cheaper than a regular policy. Consider a family floater plan only when you are married and have kids; don't include your parents because the premium is determined by the age of the oldest member. Also, don't just consider low premium as a criterion. Look at the claim settlement ratio, hospital network, inclusions and benefits before buying a plan. Critical illness plan "This provides a lump-sum benefit in case of certain pre-decided ailments and pays the costs associated with longterm care and loss of income due to prolonged recovery period," says Jacob. It is available both as a standalone policy or as an add-on with life and health insurance. Typically a standalone plan will offer a higher cover and more flexibility. You can avoid buying it at this stage, but consider it in your 30s given the higher incidence of such diseases at lower ages. Accident disability plans This is a plan you should buy when you start working because of the sheer unpredictability of life. It covers you against mishaps that can result in complete or temporary loss of income due to partial or total disability. Buy a cover for Rs 20-25 lakh or one in accordance with your income and nature of job. Home contents plan Though you are unlikely to have a house at this stage, buy a policy for the contents if you are in another city, not with your parents. The premium for a Rs 5 lakh cover can be Rs 3,000 and will cover jewellery, home appliances, furniture, etc, against theft, fire and natural disasters. Do you know which cover you need?

Harshinder Kaur 27 years, Ganganagar (Rajasthan) Designation: BankerStarted work at 25 years

Flying start 1. Complete clarity on goals. 2. Has health and critical illness insurance plans. 3. Clued in about insurance, taxation. Take-off troubles 1. Has no budget. 2. Has no equity investment except in the NPS. 3. High investment in tax inefficient fixed deposits. 6. IMPROVE YOUR SALARY STRUCTURE You may have had the best package in campus placement, but the salary would still seem less compared to that of your seniors at work. This is something beyond your control. What is in your hands is making the most of what the company is offering you. The government does not recognise the concept of CTC in computing for statutory heads, such as Employee Provident Fund (EPF), Employees' State Insurance, gratuity and bonus, where the rules prescribe minimum contributions, there are no set rules on structuring the CTC. The salary break-up is mostly the company's prerogative. There are broad norms, such as the basic pay being 30-40% of the salary, and house rent allowance (HRA) and other retiral benefits like the EPF being a percentage of the basic. However, these too are not written in stone. Moreover, what constitutes the CTC will vary from company to company. All CTC structures include three main components—basic, retiral benefits, allowances and reimbursements. Other components vary. Companies may or may not include variable payouts, such as performance bonus and gratuity in the 'total target remuneration'. Also, benefits given in kind, for in-wages. This means that except stance, house, furniture and car, are sometimes part of the total pay. Some companies even include premium paid for group benefits such as health and accident insurance in your CTC. So, unless you see the salary break-up and do the math, you cannot be sure about what you'll get in hand. You need to make sure that you are not losing out because of lazy salary structuring by some HR personnel. So customise your CTC according to your needs. Restructure the basic pay The basic, probably the chunk of your salary, includes basic pay, HRA and often dearness (DA) and special allowance. Apart from HRA, every component is fully taxable. An easy way to reduce tax liability is to cut basic pay and adjust it as perks or long-term benefits. If you have a special allowance component, adjust it as a tax-free component. However, you need to weigh the pros and cons before tinkering with your basic. Your HRA (usually, 40-50% of the basic) and EPF (12% of the basic) are directly linked to the basic. Also, if you want to apply for, say, a car or home loan in the short term, you may not want the basic pay to be too low. A higher basic would mean a higher HRA, DA and provident fund contributions. The DA will be taxable and the PF contributions are tax-free, but it will reduce your take-home salary. On the other hand, reducing the basic pay will mean a lower contribution towards retiral benefits, which may not be good in the long run. Also, if you live in a rented house, recalculate your tax benefits on HRA before lowering the basic. The idea, is to have an HRA as close to the actual rent you pay, which should ideally be a figure close to the HRA you receive plus 10% of you basic (see HRA calculations). Choose one of the following two ways to restructure the salary with maximum tax benefits. Increase in-hand salary Benefits such as leave travel allowance (LTA), medical and conveyance allowances serve two purposes. One, they increase the net takehome salary. Two, they make the salary structure more tax-efficient. However, the limitation is that there are caps on most of these perks. For instance, you can claim up to a maximum of Rs 15,000 every year for medical reimbursements, Rs 26,400 for food coupons, Rs 5,000 as annual gifts and Rs 19,200 as travel allowance on a yearly basis. Also, keep in mind that you will have to produce original bills and receipts to claim some of these expenses. So, make sure they are within the claimable limit. Take advantage of perquisites if you are planning to buy a car or join a professional course while working. Rather than taking a loan, if your employer funds the expense and includes it as a part of your CTC, your tax outgo can reduce significantly. This is because you are taxed only on the perk value. For instance, if you plan to buy a Rs 6 lakh car on loan, you will have to pay roughly a monthly EMI of Rs 13,000 for five years, which will be a post-tax expense. The tax outgo over five years on Rs 7.8 lakh will be slightly more than Rs 2 lakh. However, if the company shows it as a perk, you are taxed only for the perk value of the car, which is between Rs 1,800 a month (for cars of up to 1600 cc) and Rs 2,400 a month (for cars bigger than 1600 cc). The only disadvantage is that, legally, you don't own the car. But when you quit, you may request the company to allow you to buy the vehicle at depreciated cost. This rule holds true for other big ticket expenses like laptop, gadgets, except in case of rented accomodation. When it comes to a 'company leased house versus selfrented accommodation', HRA wins. This is because rather than getting a tax-exemption for HRA, a prerequisite value (rent paid or 15% of the basic, whichever is lower) will get added to your taxable income, which would mean a higher tax bill. Optimise long-term savings If you want to keep your basic intact but do not mind a slightly lesser take- home pay, reduce your allowance and increase your retiral benefits to reduce your tax liability. The employer's contribution to PF is linked to your basic (12%) and unalterable. However, you can increase yours using the voluntary provident fund (VPF) route. VPF is even better than PPF because while both earn similar returns, PPF has a lock-in period of 15 years. Your EPF contributions can be withdrawn without any tax implication after five years of service. If tax liability is not nil after exhausting the Section 80C investment limit of Rs 1.5 lakh, contribute towards NPS to claim an additional Rs 50,000 deduction under the new Section 80CCD (1b). "An employee's contribution is also considered as a self-contribution and therefore eligible for deduction under Section 80CCD (1b). One can first maximise his claims under Section 80C and then claim any residual under the new section," says Archit Gupta, founder and CEO, ClearTax.in. NPS, however, does not enjoy as high a liquidity as PF. Withdrawal is only allowed at retirement or under special circumstances. Not all long-term benefits are tax-efficient, and you may want to get rid of a few as well. For instance, gratuity, another common long-term benefit is tax-free up to 15 days of basic pay or Rs 10 lakh, whichever is lesser. However, it is payable only after five years of service. So, it is redundant if you do not plan to stick around for so long. Although not a very big component, you should try and adjust the money under some other head. Tax and tweaks A quick checklist of tax rules for major components and how to tweak them to get maximum benefits.

Investing the savings If you have an education loan running, paying it back should be your priority. You get a tax benefit under Section 80E for paying the interest back. Also, financial planners suggest prepaying a loan after the moratorium period rather than investing as there will be no prepayment charges. "If this your first job and your basic is higher than Rs 15,000, you may even consider opting out of the EPF and instead pay back the loan," says Vaibhav Sankla, Director, H&R Block India. "It is better better to pay back a loan where you are paying 12-13% interest than invest in an instrument that fetches you 8.7% returns," he adds. Prepaying in the earlier years is a tax-efficient strategy as well, when the interest component is higher. This is because there is no cap on how much you can claim under Section 80E. However, you have a time limit of eight years to claim this benefit. Another benefit that people living with family miss on is HRA. Even if you are living with parents, you can claim a deduction for house rent, provided your parents own the house. They will be taxed on this, but can claim a flat 30% of the annual rent as deduction for maintenance expenses such as repairs, insurance, etc., irrespective of the actual incurred expenditure. So, if you pay Rs 12,000 a month, your parents will have to pay tax on only Rs 1 lakh. Even if this earning is above the the basic Rs 2.5 lakh exempt limit (Rs 3 lakh if they are above 60 and up to Rs 5 lakh if above 80 years of age), you can make it tax-free. "The amount above the basic exemption limit can be invested in their name under tax-free Section 80C options" says Sudhir Kaushik, Co-Founder & CFO, Taxspanner.com.

Then: 1. If HRA = Rent paid (Rs 12,000), the maximum deduction you can claim is Rs 9,600 (rent paid less 10% of basic). So, you pay tax on Rs 2,400. 2. If HRA > Rent paid (Rs 10,000), the maximum deduction you can claim is Rs 7,600 (rent paid less 10% of basic). Here, the tax liability is even higher. You pay tax on Rs 4,400. 3. If HRA< Rent paid (Rs 15,000), the maximum deduction you can claim is Rs 12,000 (actual HRA). Here you are paying a higher rent (Rs 3,000) than actual HRA and therefore losing on tax benefits. 4. If HRA < Rent paid (HRA+10% of basic is equal to Rs 14,400), the maximum deduction you can claim is Rs 12,000 (actual HRA). This is ideal. **How young earners can grow their salary with their career** 7. SAVE FOR AN EMERGENCY Caught in the thrill of making money, the urgency to buy things and eagerness to save for bigger goals like a house and a car, the new earners typically forget the preparation for financial emergencies. Be it the sudden loss of job, medical eventuality or sudden financial support required by a family member, you will need to be ready for contingencies. So the first thing to do, even before you start saving for smaller, short-term goals, is to build an emergency corpus. This should be equal to 3-6 months of your household expenses, and should also include any loan repayments and insurance premium obligations. This amount should be invested in such an avenue that it is easily accessible and is not subject to market fluctuations. "The best option is to put it in a short-term debt fund, liquid fund or a sweep-in bank account. This will ensure easy availability and higher rate of interest for your money," says Maalde. Some people also prefer to use credit cards to tide over financial emergencies, but remember that these are useful only if you restrict the credit to one month. Otherwise, the cost of loan will be prohibitively high and defeat the purpose. So, before you go on a spending spree with your pay cheque, save the amount for a rainy day.

Saugata Palit, 24 years, Delhi Designation: Senior executive Started work at 23 years

Flying start 1. Budgets using Excel sheet. Has short-term goals. 2. Has adequate health insurance. 3. Has high credit score. Take-off troubles 1. Fully invested in debt. 2. Has included parents in a family floater plan. 3. Low exposure on investment tools. Also Read: How young earners can grow their salary with their career 8. AVOID DEBT TRAPS You are probably the most vulnerable when it comes to debt traps as you start working. With few responsibilities and the new-found power of money and credit card, it's difficult to curb the consumerist urges. As Pai says, "You should understand the difference between needs, wants and greed." Credit card is not the only path to debt hell. Here are the various ways you can plunge into liabilities when you start working: If you roll over credit card dues "When I started earning, I had a card with a limit of Rs 40,000, but I got so carried away that once I spent Rs 45,000 in a month. That was a wake-up call. I repaid the amount and stopped using the credit card," says Palit. He hasn't carried out a single credit card transaction in the past six months. Nayyar, on the other hand, has avoided this situation with discipline and smart usage. "I use a mix of credit and debit cards. The credit card is used only to earn and redeem points," says Nayyar. He also makes sure to pay the entire bill every month and has never rolled over the due amount. This is a cardinal rule for credit card usage. Do not roll over the due amount and repay in full because the cards charge a very high interest of nearly 3% a month. So if you get a bill of Rs 10,000 and pay only the minimum due amount of 5%, you will have to pay an extra Rs 21,978 after a year. "Fix a spending limit for yourself, say, 20% of your income. But if you can't discipline yourself, use a debit card," advises Jhaveri. "There are so many lucrative offers on cards that people don't think twice about taking these up. Avoid buying expensive gadgets on loan even if these comes with 0% interest offers. These will add up and impact your other investments," says Iyer. If you take too many loans The easy option of buying on credit can be your downfall if you do not set limits. Taking a personal loan while running loans for a car and a home can strain your finances, making it difficult to invest or save. As a rule, do not spend more than 40-45% of your income on loan repayments. Of this, 25-35% should be for home loan repayment and the rest for other forms of debt, including car and credit card loan. If you take personal loan for spending Given the ease of securing a personal loan with pre-approved amounts, it is easy to give in to the urge. Know that personal loan is one of the most expensive forms of loan after credit cards and charges 20-24% interest per annum. Avoid these at all cost. If you buy a house with high EMI Buying a house is a dream for most new earners, but consider several factors before taking the big decision. "Know the difference between fixed and floating rate loans and understand how EMIs are calculated," says Pai. Understand that the EMIs for a home loan are big and a long-term commitment. So you need to be sure of your earning capacity on a sustained basis, otherwise it will turn into a liability that will impact all your other goals. If you sign on as a guarantor for a loan When you are single and employed and have friends you can't refuse, you can be an easy target for a debt trap. If you sign on as a guarantor for a friend's loan, understand that if he cannot repay the loan, you will be asked to do so. The guarantee amount will show as outstanding liability in your credit card and affect your loan eligibility. So think twice before agreeing to such an arrangement. If you don't budget If you fail to keep track of your expenses on a monthly basis, there is a good chance that you will run out of funds before the month ends. You may then have to consider loans to fulfil your needs.

25 ideas for Budget 2018 to make common man's personal finance less taxing

As the Finance Minister and his team sit down to frame the Budget, ET Wealth has a few suggestions.

Will the Budget bring down taxes? This is probably the most-asked question in the weeks before the Finance Bill is tabled in Parliament. But though we are a nation obsessed with tax, the startling fact is that only 3% (4.1 crore Indians) of the total population filed income tax returns in 2014-15. Only 1.6% actually paid income tax. One out of two Indians who filed a return declared zero taxable income. Even so, the budget proposals relating to tax slabs, deductions and exemptions are very closely watched by Indians, almost as if the Budget is only about personal taxation. In the previous Budget, nearly everybody had expected that the finance minister will offer significant tax relief to the middle class to act as a balm after the searing pain of demonetisation. However, though the Budget did reduce the average taxpayer's tax burden, it also took away some benefits. The cap on the deduction of home loan interest was a major shock for those with houses put out on rent. This year, the expectations of a taxpayerfriendly budget are even higher, given that five states have assembly elections in 2018 and another three in 2019. Many economists fear that the government will roll out a populist Budget. As the Finance Minister and his team sit down to frame the Budget, ET Wealth has a few suggestions. We have short-listed 25 measures that experts from the financial services industry would like to see in the Finance Bill, 2018. Admittedly, some of these measures, like a longer tenure for education loan deduction, a separate deduction limit for pure protection term plans or making NPS investments tax free, will have an impact on revenue collections. The government, already under pressure to rein in the fiscal deficit, may not be able to introduce all such measures. But most of the other steps will not have any significant impact on revenue collections. They will only make life easier for common taxpayers, investors and consumers. 1) Increase duration for education loan deduction Under Section 80E, the interest paid on an education loan from a qualified lender can be claimed as a tax deduction. But this benefit is available only for a maximum of eight financial years. When this deduction was introduced in 2006, a four-year engineering course cost around Rs 3-4 lakh and a medical degree cost around Rs 5-6 lakh. The cost of higher education has risen quite sharply since. Today, an engineering course costs Rs 8-9 lakh and a medical degree roughly Rs 12-14 lakh. The prevailing interest rates for education loans range from 10.5% to 13.5%. Assuming a rate of 11.5%, the EMI for a loan of Rs 25 lakh for eight years will come to around Rs 40,000. The average borrower may have to extend the loan well beyond eight years. So the window for tax deduction should also be widened. Just like a home loan, it should be available for the full tenure of the loan. This would encourage young Indians to seek top-grade education and build a strong foundation of human capital.

RAJ KHOSLA, FOUNDER AND MANAGING DIRECTOR, MYMONEYMANTRA.COM

2) Raise limit for tax deduction for NPS contribution by self-employed Under Section 80CCD (1), there is a cap on the tax deduction that self-employed taxpayers can claim on contributions to the NPS. The 2017 Budget had increased this cap from 10% to 20% of gross income, to bring in parity between salaried and self-employed taxpayers. However, for self-employed taxpayers this comes under the overall deduction limit of Rs 1.5 lakh under Section 80CCE. On the other hand, an employee can claim deduction for up to 10% of his income under Section 80CCD(1) within the overall limit, and a further deduction of employer's contribution of up to 10% of salary under 80CCD(2), without any overall limit. To bridge this gap, the overall limit for self-employed taxpayers should be raised to match the benefits available to salaried employees. The government should consider raising the limit under Section 80CCE to say Rs 5 lakh or 20% of the gross income. This will encourage self-employed taxpayers to invest more in NPS.

ASHISH GUPTA, CHARTERED ACCOUNTANT 3) Abolish dividend distribution tax The dividend distribution tax (DDT) discourages companies from paying dividends, which dampens investor confidence. The DDT should be removed to improve investor sentiment. There is also a need to amend Section 14A, Rule 8(d), which seeks dis-allowance of expenses. Inclusion of divided in 'exempted' income is misleading and untrue because dividends are already taxed under DDT.

K. SURESH, PRESIDENT, ASSOCIATION OF NATIONAL EXCHANGES MEMBERS OF INDIA 4) Bring back standard deduction for salaried class The Finance Minister indicated that there are plans to reduce corporate tax rates this year, as in previous budgets. He should also consider reducing the individual tax rates or increasing slab limits. While others are paying tax after the deduction of expenses, the salaried class is obligated to pay tax at the gross level. This is an unfair arrangement. The best way to resolve this is to bring back 'standard deduction'. A flat standard deduction percentage can be fixed for the salaried class, thereby restoring equity between them and other taxpayers.

ASRUJIT MANDAL, PARTNER, BDO INDIA 5) Retain long-term capital gain tax benefit on equities Some entities, mostly stock brokers, are demanding a repeal of the securities transaction tax (STT) and simultaneous withdrawal of tax free status of long-term capital gains from equities. While a reduction in STT is welcome, there is no need to link it with the tax-free status of long-term capital gains. If this facility is withdrawn, it will deal a blow to the appeal of equities, which has started gaining traction. Since the risk capital is a basic necessity for economic development, withdrawing this benefit can also impact economic growth, and in turn, overall tax collection. In fact, tax loss from this move may be higher than that of the tax forgo happening due to tax-free long term capital gains.

SANJAY SINHA, FOUNDER, CITRUS ADVISORS

6) Facilitate donation and gifting of investments The tax laws need to be changed to allow donation and gifting of securities, such as listed stocks and mutual funds, without tax implications. The value of the gift or donation could be calculated as the fair market value of the securities on the date of actual transfer. This would give the donor or gift giver two benefits: exemption from capital gains tax on the securities; and tax-deduction on the amount from their income. Right now, the process of gifting or donating an amount invested in securities involves liquidating them and transferring the cash amount. The process leads to the investor incurring capital gains tax. Changing this would not only promote the practice of gifting investments, but also allow people to donate to worthy charities without worrying about taxability.

KUNAL BAJAJ, FOUNDER & CEO, CLEARFUNDS 7) Reduce GST on insurance products from 18% to 5% The goods and services tax (GST) has simplified the cascading tax structure and reduced tax rates for a host of products and services, thereby reducing the burden on end consumers. However, the tax bracket on financial services has been hiked from the initial 15% to 18%. This has made life insurance products costlier, especially pure protection and endowment plans. India has one of the highest protection gaps in Asia, with an abysmally low life insurance penetration of 3-4%. In the absence of a comprehensive social security mechanism, insurance provides the first layer of financial security to an individual or family. It is, therefore, imperative to exempt insurance products or subject them to 5% GST. Ideally, pure protection life insurance and health insurance should be considered as "essential" services and completely exempt from tax.

ASHISH KUMAR SRIVASTAVA, MD & CEO, PNB METLIFE INDIA INSURANCE 8) Reduce LTCG holding period for REITs Real estate investment trusts (REITs) can increase the depth of the real estate market by offering a new asset class for investors as well as provide a credible exit route for existing investors and developers. They have the potential to enhance the supply of commercial real estate—an enabler for the employment ecosystem. But though REITs have received regulatory approval, this potent instrument of change in the real estate industry has been held back. Despite being like debt instruments which offer close to stated returns, REITs carry an inherent element of risk which makes them similar to equity investments. The risk profile of REITs is somewhere between those of debt instruments and equity. The budget needs to cut down the long term capital gains holding period for REITs from three years to one year. This would bring the investment opportunity at par with equity investments and would make REITs more palatable to investors.

SHISHIR BAIJAL, CHAIRMAN & MANAGING DIRECTOR, KNIGHT FRANK INDIA

9) Hike tax-free limit for medical allowance There has been a marked increase in the incidence of communicable and lifestyle diseases in India, driven by unhealthy eating habits and lifestyles. To make matters worse, there has been a steady rise in medical inflation, which is currently growing at 18-20% per annum. So, the medical expenses of the average household can easily exceed the medical allowance limit of `15,000 per year. Health insurance policies normally don't cover expenses like consultation fees, medicines and diagnostics, and individuals have to shell the extra amount out of their own pocket. Companies usually cap the medical allowance at the tax free limit of Rs 15,000. If this limit is revised upwards, companies will also be encouraged to hike the allowance.

SANDEEP PATEL, CEO & MD, CIGNA TTK HEALTH INSURANCE 10) Make home insurance mandatory and offer tax deduction on premium The memory of the Mumbai floods is still fresh in the minds of the city's residents. While the trauma was unavoidable, a home insurance policy could have saved many from financial stress. To make home insurance pervasive, there needs to be a concerted effort from all stakeholders including the government. The government should make home insurance compulsory and incentivise home buyers by providing income tax benefit for the premium paid towards a policy. This will not only ensure protection against financial loss for customers, but will also aid in deepening insurance penetration in the country.

K.G. KRISHNAMOORTHY RAO, MD AND CEO, FUTURE GENERALI INDIA INSURANCE 11) Introduce individual retirement account Instead of compelling investors to keep track of multiple schemes and sections to make the most of the existing exemptions under 80C, the government should introduce a separate Individual Retirement Account (IRA). It should allow a certain percentage of income to be tax free as long as it is allocated to the IRA and not withdrawn for a lock-in period of 20-30 years. The investor should be free to choose any asset class to invest in and reallocate at will.

VIKAS GUPTA, CEO & CHIEF INVESTMENT STRATEGIST, OMNISCIENCE CAPITAL 12) Include low-risk hybrid funds under Section 80C Many investors invest in FDs to reap taxation benefits under Section 80C. But due to the falling interest rates, they are looking for options that promise better returns, relatively lower risk and the same tax advantage. For conservative or first time investors, the best alternative is hybrid funds. Hybrid funds are designed to generate good returns through investment in equities, while protecting the downside and smoothening volatility through investment in debt. For low-risk investors, hybrid funds offer higher returns compared to traditional options and are less volatile than equity oriented funds. Hence, the 80C tax exemption benefit should be extended to this category, with a lock in of 3 years like ELSS.

RADHIKA GUPTA, CEO, EDELWEISS ASSET MANAGEMENT 13) Reduce holding period for LTCG from debt funds To encourage retail investors to invest in debt funds and to standardise the holding period across various asset classes, the minimum holding period for long-term capital gains should be reduced from 36 months to 12 months. This will bring debt funds on par with equity schemes and other instruments like listed corporate bonds. The LTCG may be retained at 20% with indexation benefit, but the tax rate for long-term investments of over 10 years in debt oriented schemes should be reduced to 10%. This would encourage investors to remain invested for longer periods and build their corpus.

BEKXY KURIAKOSE, HEAD - FIXED INCOME, PRINCIPAL PNB MUTUAL FUND 14) Change tax rules for vesting date of stock options Employee Stock Option Plans (ESOP) become taxable as a perquisite on the allotment or transfer of shares. However, with growing complexities in plan designs, such shares may be subject to a further lock-in period after they have been allotted or transferred. This tax incidence should be postponed until the lock-in period expires. The previous Budget had proposed that specified tax exemption would not apply to the sale of equity shares purchased after 1 October, 2004, without the payment of STT. Subsequent notifications provided some relaxation for ESOPs and Employee Stock Purchase schemes, but, it is not clear if this exemption is available for shares of unlisted companies, which are subsequently listed. The Budget should clear the air on this issue.

HOMI MISTRY, PARTNER, DELOITTE INDIA 15) Make tax return filing automatic for individuals

Taxpayers already use online portals for tax filings, wherein personal and tax paid information are pre-populated in the tax form. The government can take this a step further by sending pre-populated tax forms to taxpayers with information from their Form 26AS and other financial transactions linked to their Aadhaar and PAN. The taxpayer should have the option of reviewing and modifying the information before filing. This automatically generated tax return should be considered final unless the taxpayer modifies it before the due date. There will be a small number of people who will need to modify their information further to report Indian or foreign assets and claim of double taxation relief. While the process might involve implementation challenges, over the long term, it will ease the burden of compliance and therefore bring down tax rates for all taxpayers.

ABHISHEK GOENKA, LEADER CORPORATE & INTERNATIONAL TAX, PWC INDIA 16) Tax developers for unsold inventory to bring down real estate prices The government has already taken several steps to make housing affordable. However, affordability is still an issue in India due to high real estate prices. Some restrictive policy actions in the Budget can help rationalise property prices. Though demand is low, prices are still high because builders and high net worth investors refuse to divest of their inventory. The Budget should introduce a 10% tax on holding on to inventory after all aspects of building construction are complete , and the occupation certificate has been obtained. This will compel builders to reduce inventory in finished projects and the increased supply will bring the prices down. However, the impact of this move will last only as long as the existing inventory does.

PANKAJ KAPOOR, MD, LIASES FORAS

17) Reduce import duty on gold to align with GST Gold has been assigned a special GST slab of 3%. However, the high customs duty of 10% promotes an active grey market in the metal. For broader financial reforms to succeed, and in order to lift gold's economic contribution, the metal must be brought into the mainstream. To this end, overall tax on gold needs to be rationalised with a substantial reduction in customs duty.

SOMASUNDARAM P.R., MANAGING DIRECTOR - INDIA, WORLD GOLD COUNCIL

18) Make holding period uniform for all tax savings products At present, investors can avail of tax benefits subject to different lock in periods, based on the nature of underlying investments. For instance, ELSS have a lock in of three years, whereas the tenure for availing of long term capital gains tax benefit is one year for equity investments, and three years for debt investments. For bank FDs it is five years and different for EPF and PPF investments. Aligning the tax benefits based on longevity of investments, rather than on the underlying asset class, would better enable investors to decide their risk appetite without any tax biases in mind.

SANJAY SACHDEV, CHAIRMAN, ZYFIN HOLDINGS 19) Make pension plans tax friendly According to an RBI report, only a small number of Indians above 65 years of age have saved in private pension plans and a large segment of the total population has not taken any steps to ensure adequate financial coverage during retirement. One major reason for this is the taxability of pension plans. Right now, if an investor does not buy an annuity on maturity, 66% of the corpus is taxed. Even the pension from the annuity is treated as income and taxed accordingly. Both these tax rules should be relaxed to encourage people to invest in pension plans.

TARUN CHUGH, MD & CEO, BAJAJ ALLIANZ LIFE INSURANCE 20) Separate tax deduction for pure term plans At present, there is a significant amount of overcrowding in the Section 80C basket. In order to remedy this, the insurance industry has repeatedly sought a separate tax deduction limit for life insurance plans. If this is not possible, a separate deduction should be offered for pure protection term plans. In India, tax benefits often drive financial decisions. Therefore, a separate limit is likely to encourage a lot of taxpayers to buy term insurance.

ADHIL SHETTY, CEO AND CO-FOUNDER, BANKBAZAAR.COM 21) Cut GST rate for property from 12% to 5% The GST rate for real estate is 12% of the sales consideration. Before GST, the service tax was around 4.5% and value added tax was 1%, taking the total tax outgo to 5.5%. Now the input tax credit is available on taxes paid on the purchase of construction materials, which can be the adjusted against the GST liability. Even after this adjustment, the effective tax rate is significantly higher, and the stamp duty is still applicable, which increases the costs for the consumer. State governments should abolish stamp duty or align it with the GST rates.

SURENDRA HIRANANDANI, CMD, HOUSE OF HIRANANDANI 22) Offer tax relief to senior citizens Falling interest rates have hurt senior citizens who may not have the risk appetite for equityoriented instruments. To cushion the impact, senior citizens with an income of up to Rs 10 lakh per annum should be offered a deduction of Rs 75,000 towards interest on fixed income instruments. In addition, they may also be allowed a deduction of Rs 50,000 for their routine medical expenses.

KULDIP KUMAR, LEADER, PERSONAL TAX, PWC 23) Let NRIs claim deduction for treatment of relatives The tax rules for NRIs are quite different from those that apply to residents. The process of tax reporting is very elaborate, the TDS rules are quite stiff and they don't enjoy some of the tax privileges that normal citizens are eligible for. For instance, NRIs are not eligible for tax deductions for the medical treatment of a disabled dependent under Section 80DD, or the treatment of a family member suffering from a specified diseases under Section 80DDB. The Budget needs to fix this anomaly. If an NRI is paying for the treatment of relatives in India, he should be eligible for the same deductions that residents are.

SUDHIR KAUSHIK, CA & CO-FOUNDER, TAXSPANNER.COM 24) Let Aadhaar linkage act as centralised KYC Carrying out multiple KYC compliance processes is a major pain point, not only for investors and investors, but also for financial services companies. Bank accounts are already linked to a holder's PAN and will soon be linked to their Aadhaar as well. This will automatically verify the identity of the investor. Aadhaar linkage should be treated as a centralised KYC, so that the investor does not have to repeat the process.

VIKASH JAIN, CO-FOUNDER, SHARE SAMADHAN

25) Up to 60% of the NPS corpus should be made tax free In recent years, the government has offered various tax sops for investing in the National Pension System (NPS). Even so, the pension scheme has not seen the desired success as was anticipated by the government. Much of this is due to the tax treatment of the NPS corpus at the time of retirement. While 60% of the corpus can be withdrawn at the age of 60, only 40% is tax free and the remaining 20% is taxed as income. This is a major dampener while evaluating NPS as an investment option. The Budget should review the current provisions for taxing the NPS if the government wants to encourage people to opt for the scheme and make India a pensioned society.

DIVYA BAWEJA, PARTNER, DELOITTE INDIA

0Comments

Subscribe & get the Latest Personal Finance updates delivered to your mailbox.

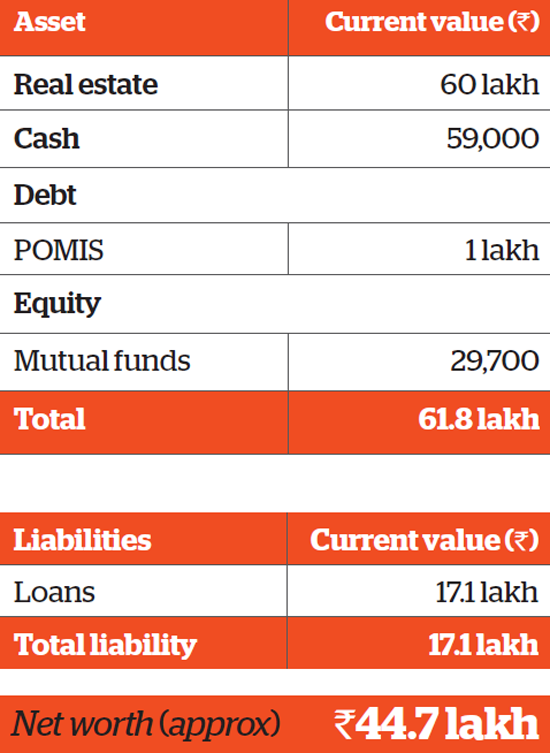

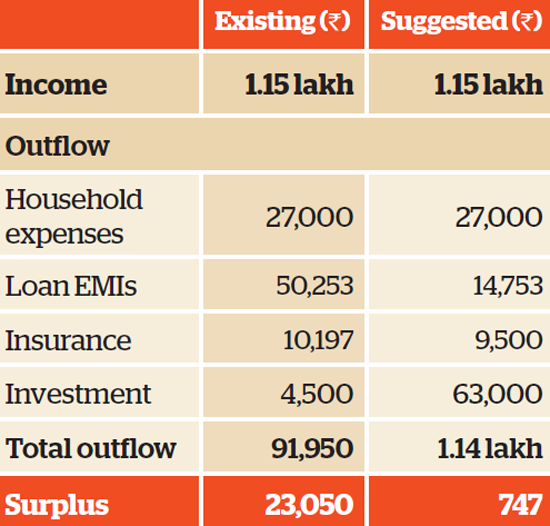

Mumbai-based Murali Krishnan works in the IT industry and lives with his wife, Megha, 42, and two kids aged 14 and 8. He brings in a salary of Rs 1.75 lakh and also gets a rental income of Rs 35,000. He has three houses and a plot of land, and has taken a home loan of Rs 46 lakh. After household expenses, insurance premium, contribution to parents and a home loan EMI of Rs 52,100, he is left with a surplus of Rs 74,258. His goals include saving for emergencies, kids' education and weddings, and retirement. Portfolio

Cash flow

Financial Planner Pankaaj Maalde suggests Krishnan start by building an emergency corpus of Rs 12.4 lakh, which includes a medical buffer of Rs 5 lakh for his parents. He can allocate his fixed deposit and cash holding for this goal. For his older son's education, Krishnan needs Rs 32.7 lakh in four years. For this, he should start an SIP of Rs 60,000 in an equity income fund. For his younger son's education, he needs Rs 64 lakh in 10 years. How to invest for goals

Annual return assumed to be 12% for equity. Inflation assumed to be 7%.

To meet this, he should allocate his stocks and equity funds and will also need to start an SIP of Rs 20,000 in a diversified equity scheme. For his children's weddings in 11 and 17 years, Krishnan needs Rs 73.5 akh and Rs 1 crore, respectively. He should rely on his plot of land to meet these goals and will not need to invest any more. For retirement, Krishnan will need Rs 3.5 crore and can assign his EPF corpus as well as two houses for the goal. He doesn't need to invest any further. For life insurance, Krishnan has one traditional plan and two Ulips. Maalde suggests he retain the former and review the latter after the lock-in period of five years. Though these plans offer a low cover, the needbased theory suggests that Krishnan doesn't need to buy any more life insurance as he has sufficient number of assets. Since his wife is not earning, she too doesn't need any life insurance. For health insurance, his employer provides a cover of Rs 6 lakh. Maalde advises that he buy a Rs 20 lakh family floater plan independently and this will cost him Rs 3,333 a month in premium. Insurance portfolio

Premiums are indicative and could vary for different insurers.

Financial plan by Pankaaj Maalde Certified Financial Planner

Write to us for expert advice Looking for a professional to analyse your investment portfolio? Write to us at etwealth@timesgroup.com with 'Family Finances' as the subject. Our experts will study your portfolio and offer objective advice on where and how much you need to invest to reach your goals.

Personal finance disruptions of 2017 and takeaways for 2018

From introduction of penalty for late filing of income tax returns (ITR), increasing use of Aadhaar, to the decline in interest rates, there were many events that disrupted the working of our personal finances in 2017. Here's a flashback and pointers to help you incorporate these changes in your financial plans for 2018. 1. Income tax changes In the Budget 2017, the government slashed the tax rate for individuals in the lowest income tax slab - Rs 2.5 lakh to Rs 5 lakh -to 5% from 10%. Further, the rebate under Section 87A of the Income-tax Act, 1961 was reduced to Rs 2,500 from the Rs 5,000 for those earning between Rs 2.5 lakh and Rs 3.5 lakh. Earlier, those earning up to Rs 5 lakh were eligible for this rebate. It was also announced that those earning between Rs 50 lakh and Rs 1 crore will have to pay a surcharge of 10 percent on the total income tax payable by them. Takeaway for 2018: Remember to calculate your taxes using the new tax structure and rebate changes when filing your return for FY2017-18 in 2018. 2. Penalty for filing ITR after the due date In the budget, the government had also introduced a maximum penalty of Rs. 10,000 for delayed filing of ITR by individuals. This fee is applicable with effect from April 1, 2018. As per the new rules, the fee to be levied is based on the time period of delay which is as follows:

(i) A fee of Rs 5,000 in case returns are filed after the due date, but before the December 31 of the relevant assessment year or (ii) Rs. 10,000 in case it is filed after December 31 of the relevant assessment year. Takeaway for 2018: Earlier there was no specific penalty for delayed filing of income tax return (the penalty was for late payment of taxes). So, now that there is a penalty for returns filed beyond the due date, file your ITR for FY2017-18 on time and save yourself the penalty payment. 3. New classification of mutual fund schemes The Securities and Exchange Board of India (Sebi) asked fund houses to classify their schemes into clearly defined categories. For long, there were no clear guidelines to categorise mutual funds. Since fund houses launched multiple schemes under each category, the comparison and selection was a taxing task for many investors. "It is desirable that different schemes launched by a Mutual Fund are clearly distinct in terms of asset allocation, investment strategy etc. Further, there is a need to bring in uniformity in the characteristics of similar type of schemes launched by different Mutual Funds. This would ensure that an investor of Mutual Funds is able to evaluate the different options available, before taking an informed decision to invest in a scheme," the Sebi circular said. As per the Sebi directive, the schemes would be broadly classified in the following groups: a. Equity schemes b. Debt schemes c. Hybrid schemes d. Solution-oriented schemes e. Other schemes With the new classification norms and distinct categorisation, investors will have a better understanding of the scheme and make an informed decision. Takeaway for 2018: You will know what exactly you are investing in and it will make selecting a fund easier. If a scheme says it is a large-cap fund, it will have to invest in only large-cap stocks and not a selection of large-, mid-, and small-cap stocks (in other words, a multi-cap scheme). Asset management companies will have to align their schemes to comply with the directive and make sure that they are true to their mandates. We could see mergers of schemes if the fund house has similar schemes. 4. Cut in small savings schemes interest rate The interest rate on small savings schemes like National Savings Certificate, Sukanya Samriddhi Yojana, Kisan Vikas Patra (KVP), and Public Provident Fund (PPF) went down over the last one year, albeit marginally. The interest rate on the post office savings account was retained at 4 per cent. Despite the decline in rate of interest, these small savings schemes haven't waned in popularity mainly because the interest offered on them is still higher than what is being offered by bank fixed deposits. Not only do these schemes offer competitive rates of interest in comparison to other fixed income instruments such as bank fixed deposits, some even come with tax benefits under Section 80C of the income tax Act.

Takeaway for 2018: Despite reduction in interest rates, small saving schemes still offer interest rates higher than most comparably safe bank fixed deposits. So keep these on your radar when looking for safe fixed income investment options. 5. GST on financial services The implementation of the new indirect tax regime has undoubtedly impacted your pocket, especially when it comes to financial services. From the previous 15 percent rate, banking and insurance services will attract 18 percent GST. The 3 percent hike in the tax rate has made these financial services dearer. Although service tax on mutual fund returns has increased 3 percent, the impact on returns will be marginal. This is because GST is levied on a scheme's total expense ratio (TER). Expense ratio is the measure of the cost incurred by an investment company to operate its mutual fund. Now, real estate is still not a part of GST, but construction activities including residential structures will attract GST of 12 percent. This makes under-construction projects costlier than ready-to-move-in properties. As per the Central Board of Excise and Customs, "Sale of building is an activity or consideration which is neither a supply of goods nor a supply of services." This makes the ready-to-move properties lucrative compared with under-construction properties. Takeaway for 2018: Formal sector services are getting expensive due to higher GST and it looks like this scenario is here to stay. So make sure you try to get the maximum discount on the service and avoid penal charges for late payment etc., as this will reduce the tax payable on the service charge correspondingly. 6. Cut in interest rates on savings account As a result of demonetisation, banks witnessed a surge in deposits. Reportedly 85 per cent of the currency in circulation was deposited back in banks. Going by simple demand-supply economics, this shouldn't be surprising as surplus liquidity in the banking system was at peak post demonetisation. In the recent past, a number of public and private sector banks reduced their interest rate on savings accounts from 4 per cent to 3.5 per cent. State Bank of India reduced the interest rate on its savings bank accounts, it cited decline in inflation and high real interest rates as the main reasons. Besides, the revision in rates of savings accounts has enabled banks to maintain the MCLR for loans at existing rates. Although some banks might be offering higher interest rates, they do come with caveats. Takeaway for 2018 : Don't let money idle in savings accounts - you are getting even less interest than before. Invest it instead. 7. Pension scheme with 8 percent guaranteed returns launched: Pradhan Mantri Vaya Vandana Yojana (PMVVY) is a pension scheme announced by the government in May 2017 exclusively for senior citizens aged 60 years and above. The scheme is available till May 3, 2018 and can be purchased offline as well as online through Life Insurance Corporation (LIC) of India. It provides an assured return of 8 percent per annum. payable monthly for 10 years. Pension is payable at the end of each period, during the policy term of 10 years, as per the frequency of monthly/ quarterly/ half-yearly/ yearly as chosen by the pensioner at the time of purchase. Besides, the scheme is exempted from GST. Minimum / Maximum Purchase Price and Pension Amount:

Takeaway for 2018 : As most bank FDs are currently offering lower returns, this scheme, a new entrant in the arena of government schemes in 2017, would appear of interest. However, it offers little liquidity. Click here to read and judge for yourself whether you should go for it. 8. Affordable housing push In a bid to push affordable housing, the government extended the window to avail the credit linked subsidy scheme (CLSS) on home loans under the Pradhan Mantri Awas Yojana (PMAY) by 15 months till March 2019. Besides, increase in the carpet area of houses eligible for interest subsidy under the scheme for the Middle Income Group (MIG) under PMAY (Urban) was also approved this year. The move is expected to enable the middle-income category of individuals to have a wider choice in developers' projects. Takeaway for 2018: The downslide in prices in some real estate areas and stagnancy of the same in others in 2017 has sharply reduced the attractiveness of property as an investment for people looking to make quick gains. The focus has shifted to affordable housing because of the above mentioned scheme and also because affordable housing is likely to be more saleable in the current scenario. So this is the area to watch out for in real estate in the new year. 9. Linking Aadhaar with PAN, bank accounts and various financial services made mandatory In a recent interim order, the Supreme Court said that it has accepted the government's suggestion to extend the deadline to link it with various documents and accounts by 3 months to March 31, 2018. Besides, the deadline for linking mobile phones with Aadhaar was also extended to this date from February 6. Takeaway for 2018: While the court case over whether Aadhaar infringes the right to privacy still goes on, for all practical purposes it looks like it's here to stay. So if you want a smooth financial life, link your Aadhaar to all that is required by the government if you have not already done so.

The crucial 7 years: Financial mistakes you should avoid

We hope this will not only help you become a better investor, but also enhance your riches over the years. With a little magic that the number '7' weaves for you.

As ET Wealth completes seven years this December, it's a good time to get acquainted with George Miller. In 1956, the Princeton psychologist figured out the magic of number '7'. He theorised that the number of objects an average person can remember is 7. It is probably the reason financial experts recommend that you should not have more than 7-8 funds in your portfolio. But it doesn't quite explain why equity investment for over seven years brings down the probability of loss. Or why the world is governed by 7, from the colours in a rainbow to days in a week and notes in music. Or even the reason why the proverbial seven-year itch sets in a marriage. What it has done is help us figure out the magic of number '7' when it comes to personal finance. The itches that can set in if you ignore the crucial periods of financial decision-making. The liabilities you can incur, the retirement kitty you can run out of, the mistakes that can bloat into losses, the loans that can become difficult to manage, or the children who can grow up to make flawed financial decisions because you didn't teach them money skills at the right age. These periods may not be a precise seven years, but hover around this magic number. "There are many such rules and calculations built around the number '7' in finance. For instance, it has been observed that if the market suffers a 7-10% dip, it is bound to witness a steep correction," says Priya Sunder, Director, PeakAlpha Investment Services. While we do not aim to scour for all such rules or periods, we do intend to tell you how to avoid the problems you are likely to face. Go through the following pages to understand how to take the right financial decisions during specific periods in your life, be it after getting a job or having children, after retirement or while investing in equity. We hope it will not only help you become a better investor, but also enhance your riches over the years. With a little magic that the number '7' weaves for you. ITCH 1 : QUITTING EQUITY INVESTMENT BEFORE 7 YEARS This is an itch that is consistently suffered by most investors and is well-documented. If you invest in the market in the form of stocks or mutual funds for short durations, or buy and sell erratically while trying to time the market, there is a good chance that your portfolio will be in the negative. This is because it has been proven historically that if you remain invested for at least 7-8 years, your chances of making a loss are minimal. Staying invested in equity for more than 7-8 years diminishes the probability of loss considerably, while that of making gains increases dramatically. This has been observed in an analysis of equity funds in the Indian market between 2007 and 2017, where the probability of loss reduced to zero beyond seven years. "In fact, if you look at any block of seven years in the market, you wouldn't have lost money," says Sunder. Similarly, an analysis of data from developed equity markets between 1970 and 2017, by research and analytics firm Macrobond, suggests that the probability of loss falls beyond 7-8 years and drops to zero beyond 11.1 years. "We believe that short-term investments affect behavioural decision-making and leads to emotive reactions. This means that you end up taking bad calls and fall prey to the vagaries of volatility," says Nitin Vyakaranam, Founder and CEO, ArthaYantra. "On the other hand, if you remain invested for 7-8 years, you behave in a less emotive manner. A longer-term investment also means that volatility reduces considerably, increasing your chances of gain," he adds.

"The term of investment also depends on the goal," says Jayant Pai, Head, Marketing, PPFAS Asset Management. "If you start investing when your child is born, even 15 years may not be enough depending on the corpus you need. Or if you are trying to save for retirement in 20 years, but withdraw after 7-8 years because that is the optimum investment period, that also won't make sense." So if you have long-term goals, equity may be your best bet as it will ensure that you stay on course and don't incur a loss. Investing for over 7 years cuts down the probability of loss

ITCH 2: NOT INVESTING FOR 7-8 YEARS AFTER GETTING A JOB In many ways, the first 7-8 years after you are employed and start earning are the most crucial and can decide the course of your entire financial journey. "The investor's biggest ally is time and there's no better time to start investing than to do it as early as possible," says Sunder. This is because you can take more risks, have greater flexibility to choose products, and have a better opportunity to save due to fewer liabilities at this stage in life. Besides, you can make your money grow through the power of compounding. Compounding means that the interest you earn on your savings keeps earning its own interest. For instance, if a 25-year-old starts saving Rs 2.4 lakh a year, he can build a corpus of Rs 10.9 crore in 35 years at 12% return. However, if he doesn't start investing till he is 35, then to build the same corpus he will have to increase the investment nearly three times or will amass only one-third of the corpus. That is, he will be able to build only Rs 3.4 crore instead of Rs 10.9 crore. "However, compounding can take place only if you are aware of the right instruments and invest wisely. Investors in the age group of 21-29 years typically make the most number of financial mistakes," says Vyakaranam. This means that spending and not saving may be as bad as investing in avenues like traditional insurance policies or Ulips, which lead to wealth erosion. Since it takes more time to move your investments from the negative to positive rather than vice versa, it is important that you have time on your hands to recoup the losses if you make mistakes in the initial stages. Benefit from the power of compounding

Assumptions: Current age: 30 years; Retirement age: 60 years; Rate at which savings will grow: 12%. ITCH 3: MAKING MISTAKES IN 5-7 YEARS OF RETIREMENT The period of 5-7 years after retirement is typically marked by financial mistakes. These include: Underestimating expenses If you think your expenses will fall after retirement, think again. While kid-related expenditure and debt come down, there is a rise in medical and travel costs. This may result in an insufficient corpus that may not last too long. This can also happen if you ignore inflation, which leads to wealth erosion over time. Assuming low expenses can impact your corpus

Withdrawing too much "When you get a lump sum on retirement in the form of PF or gratuity, you are under the illusion that there is lot of money. If you start withdrawing at the rate of 10%, even as the corpus grows at 7%, you will soon run out of money," says Sunder. The rise in survival rate also means that you will live longer. Hence, the need to withdraw at a rate lower than the one at which your money grows. Not diversifying Correct asset allocation is critical to ensuring that the corpus lasts longer. While you need to bring down the equity component to reduce risk, it is imperative that you invest in equity to beat inflation and make your money stretch. "Another problem is being houserich and money poor, wherein the parents may have to depend on children for money," says Sunder. Choosing tax-inefficient instruments also erodes the corpus, which is why fixed deposits may not be the best idea. Instead, go for balanced funds, which become tax-free after a year. How long will the money last if you withdraw more?

Ignoring insurance Given that there is spate in medical problems after retirement, you should review your health insurance or have a sufficient buffer. As for life insurance, you will not need it unless you have dependants or there are maturity benefits, and can end it after retiring. ITCH 4: NOT INVESTING FOR 7-8 YEARS FOR KIDS' GOALS It is important to start investing early for any financial goal; more so for children's education. If you don't start working on it in the first 7-8 years, you are likely to end up with an inadequate corpus. "It is typically the No. 1 goal for most parents, but not saving for it can impact them in so many ways since all the financial decisions are inter-connected. So if you have not saved enough for children's education, you may have to take loans and will end up increasing your liabilities," says Vyakaranam. Choosing the right instruments for investment is as crucial. "Do not buy life insurance for them, or any plan that has the word 'child' in it," says Pai. Go in for a diversified portfolio, with the right mix of equity and debt, depending on the time frame. How to invest for a child's goals The earlier you start investing, the easier it will be to reach your goal provided you choose the right instruments.

If you begin investing right after the child is born, you will have enough time to enjoy the high returns of equity funds. These are a good way to invest for children's goals as the risk is reduced considerably after seven years. They also offer high flexibility and the returns are tax-free after a year. If, however, you have delayed investment, you will have to opt for lowreturn instruments like debt-oriented funds or a recurring deposit. While these will ensure the safety of capital, you may not be able to amass the corpus you want. "If you are the sole earning member, it is a good idea to get some protection. Buying a Ulip, which also offers insurance, makes sense because it reduces the risk by ensuring that the premium is paid for even if you die," says Sunder. "Where you invest will also depend on how much money you can set aside at any given time," says Pai. If you have small amounts, go for mutual fund SIPs, but if you have a lump sum and want to buy real estate, you can do that too. But, remember not to binge on it and skew your portfolio as it is an illiquid asset. After buying the house, invest in equity. ITCH 5: TAKING CAR LOAN FOR 7 YRS OR HOME LOAN FOR 7-10 YRS Taking a loan, be it for a home or car, and the duration for which it should be taken, pose a dilemma for most investors. Some take a car loan for the maximum duration of seven years even though they can repay it earlier. Others take a big home loan for a shorter period of 7-10 years even if it strains their cash flow and doesn't leave any surplus to invest for other goals. "Repaying the loan should be top priority as peace of mind is very important. But first, you should decide on how big a house you need, the savings you have, and then pick the amount you take as loan," says Pai. Here are the other factors to help take a decision: Income: If your cash flow doesn't allow you to pay a big EMI, you will have to take a smaller loan or for a longer duration. Remember that a home loan EMI should not exceed 40% of your total income. Interest rate: If you have a lump sum of Rs 10 lakh and can either invest it or buy a car, the decision should be taken on the basis of the rate offered on the loan. "If the dealer gives you the loan at 7.5% and you can earn 12% on Rs 10 lakh, you should take the loan," says Sunder. It's also important to remember that the interest outgo keeps increasing with the tenure of the loan. So if you take a home loan for 25 years, you could end up paying over 50% of the loan as interest. How much EMI should you pay?

You pay a higher interest for a longer loan tenure If you took a home loan of Rs 50 lakh at 8.5% interest:

Tax benefit: While a home loan enjoys tax benefits, a car loan doesn't. A car is also a depreciating asset and it doesn't make sense to pay a high interest on it by taking a loan for a long duration. On the other hand, you get a Rs 2 lakh tax deduction on interest in the case of a home loan. This amount is unlimited if the house in question is rented. ITCH 6: NOT TEACHING 7-14 YEAR KIDS ABOUT MONEY It's probably one of the most important things to do during this period," says Pai. Agrees Vyakaranam: "We teach kids about everything except money. The school, too, doesn't help. This is the reason that when kids start working, they don't know what to do with their first pay cheques. The next generation is not going to have the tax incentives or optimal saving avenues that we currently do, and will need to handle the new eco-system differently." To be able to do so, parents need to start as early as possible. A recent study by the Cambridge University, England, suggests that most children's financial habits are formed by the time they are seven years old, implying that it may be too late to wait till they are in middle school to teach them money skills. However, seven may still be a good age to begin. You could start small, by giving your children an allowance and asking them to manage it. You can also teach them about basic concepts and mathematical calculations with the help of online and board games.

Graduate slowly to actual transactions, complex dealings and better habits. "The important thing is to inculcate the right value system in the child," says Sunder. "You can't preach one thing and practise another," she adds. Pai concurs. "As parents, we need to check our financial habits because kids learn by observing. So if you buy a big car that you can't afford by taking a loan, the child will assume this is the only way to do it," he says. Money arguments in front of kids may also not be a good idea as differing viewpoints will confuse the kid.

Should you buy a plot as an investment?

ET CONTRIBUTORS|

Dec 18, 2017, 06.30 AM IST

0Comments

If you have limited or no assets, beginning with a large, indivisible asset such as a piece of land could be a bad idea.

Mayank and Priya Mehra are not big savers, though they are close to 35 and have been working for over 10 years. The lifestyle choices they have made cost a lot of money and they are unwilling to cut back on expenses. While they are not servicing any long-term loans, they are not averse to borrowing money in an emergency. A friend has advised them to buy a plot of land on the outskirts of the city as an investment and develop it as a holiday home with the help of a bank loan. The idea appeals to them, since it would mean a compulsory saving to repay the loan and acquisition of an asset. Should they go ahead and buy the plot? If the Mehras have limited or no assets, beginning with a large, indivisible asset such as a piece of land is a bad idea. It may be prudent to build liquid assets in deposits, mutual funds, bonds and equity first. These assets can be sold in parts, if there is a need for money. They can also be used as collateral if a loan has to be taken. There is a psychological satisfaction in owning a piece of land whose value is appreciating, but it translates into little or no value in day-to-day living. If the idea is to create an asset (land) by allocating a compulsory monthly saving in the form of an EMI , a systematic investment plan (SIP) in a mutual fund will serve the same purpose, albeit with greater flexibility, liquidity and no interest component. They can skip an instalment if they have a problem; they can draw from the investment in case of need; and the value of their investment will also appreciate over time. A loan against the land is highly inflexible in comparison. Moreover, buying land may be extremely tax inefficient. Unless they actually construct a house on the land, they will not get the tax benefit on the principal repaid or interest paid on the loan they take from the bank. The Mehras should consider other investments instead, or buy a flat in which they could live, if they are keen on acquiring property as an asset. Content courtesy: Centre for Investment Education and Learning (CIEL).

Contributions by Girija Gadre, Arti Bhargava and Labdhi Mehta.

0Comments

Subscribe & get the Latest Personal Finance updates delivered to your mailbox.

Who will win the race to retirement: Tortoise or hare?

Even though tortoise and hare were friends, they were as different as chalk and cheese especially when it came to investments.